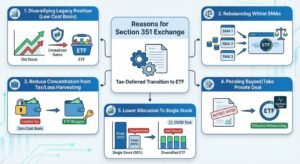

Imagine holding a stock for years, watching it appreciate 300%, only to see that position disappear from your brokerage account because a private equity firm decided to take the company private. You get a cash premium for the shares, but when a public company is acquired for cash, or a mix of cash and stock, investors often face an unwelcome surprise: an immediate, forced realization of capital gains.

There’s a sophisticated strategy to avoid this tax hit: the Section 351 Exchange into a newly formed Exchange-Traded Fund (ETF). This approach allows investors to defer capital gains, keeping their money compounding, instead of going to the IRS.

The Imminent Tax Liability from Cash Buyouts

When a stock you own is taken private or acquired in an all-cash or part-cash transaction, the deal is treated by the IRS as a sale of your stock.

- Cash Buyout: You receive cash for your shares, triggering a taxable event.

- Mixed Merger: You receive cash for a portion of your shares, forcing the recognition of capital gains on that portion.

You are immediately liable for capital gains tax on the difference between the cash proceeds and your original cost basis. This involuntary tax payment can be a major drag on returns, especially for assets held long-term.

The Strategic Solution: The 351 ETF Conversion

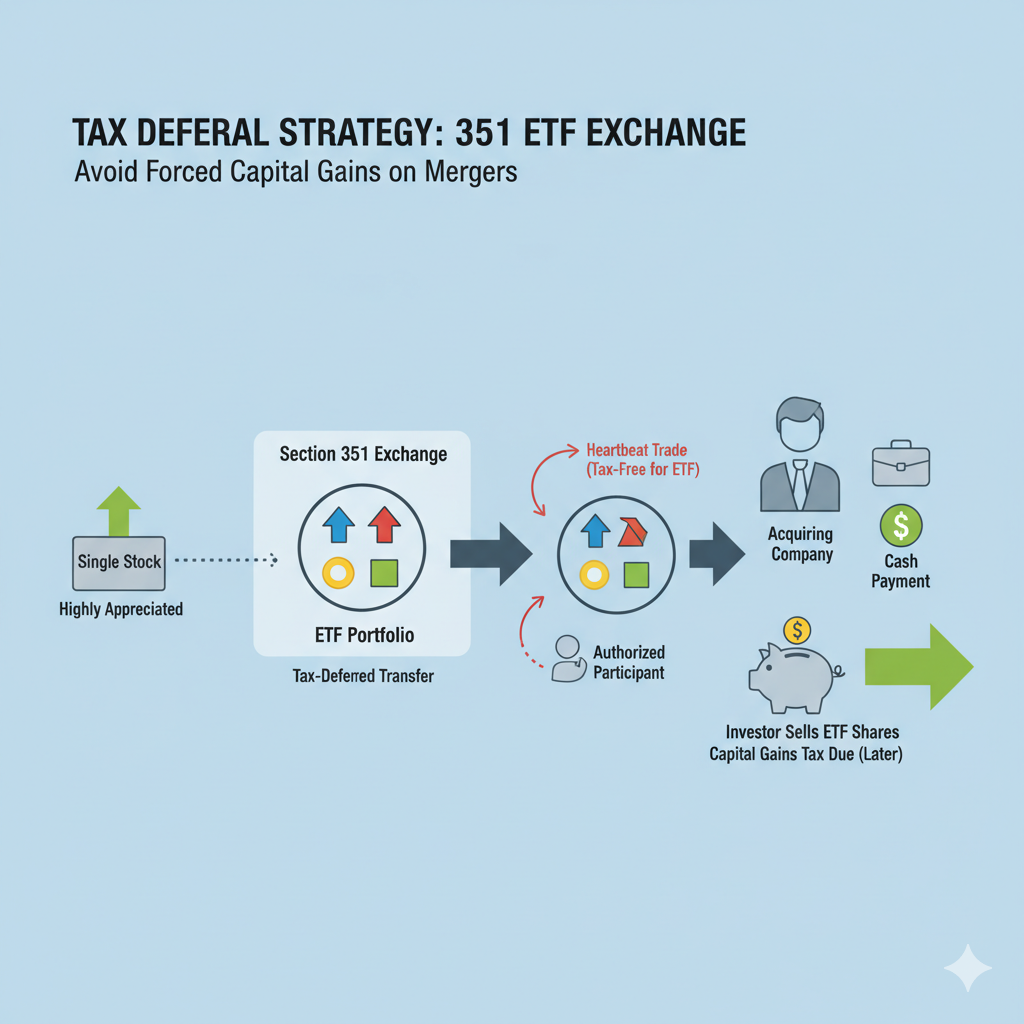

The Section 351 exchange offers a non-taxable method to transfer appreciated assets to a newly formed corporation (in this case, an ETF) in exchange for stock in that corporation. The process defers your capital gains recognition through two critical, interlocking mechanisms.

Mechanism 1: Tax Deferral from the Section 351 Exchange

The initial step is the non-taxable transfer of your appreciated stock portfolio, including the merger target shares, into the ETF.

- No Immediate Gain: At the moment of the exchange, you recognize no taxable gain or loss.

- Carryover Basis: Your original cost basis and holding period from the appreciated stocks are carried over to the ETF shares you receive. The tax liability doesn’t disappear; it is simply preserved and deferred within the ETF shares.

The Crucial Diversification Requirement

To qualify for this tax-deferred treatment, the portfolio you contribute to the new ETF must be diversified. This is defined by the 25/50 Diversification Test:

- 25% Limit: No single stock position in the contributed portfolio can exceed 25% of the portfolio’s total value.

- 50% Limit: The combined value of the stock or securities of five or fewer issuers cannot exceed 50% of the total assets.

If your merger target stock is too concentrated (over 25%), the entire transfer would fail the diversification test and become a taxable event. Therefore, this strategy works best when the target stock is a large, but not excessively concentrated, part of an already diversified portfolio.

Mechanism 2: Tax-Free Disposition by the ETF (The Heartbeat Trade)

The true genius of this strategy lies in how the ETF, now holding the appreciated merger target stock, handles the impending taxable acquisition.

Normally, if the ETF received cash for the stock in the buyout, it would realize a gain and be required to distribute that gain to its shareholders, triggering a tax event for them. However, ETFs leverage their unique tax structure, specifically Internal Revenue Code Section 852(b)(6), to avoid this.

- The “Heartbeat” Trade: Before the cash acquisition closes, the ETF manager can effectively sell the appreciated target stock without realizing a taxable gain at the fund level.

- In-Kind Redemption: This is done by distributing the appreciated merger target stock in kind to an Authorized Participant (AP)—an entity that helps manage ETF shares—in exchange for a redemption of ETF shares.

- Tax-Free for the Fund: Because this distribution is an in-kind redemption and not a sale, the ETF itself recognizes no taxable gain under Section 852(b)(6). Consequently, there is no taxable gain to distribute to you, the shareholder.

By performing this “heartbeat trade,” the ETF removes the appreciated merger target stock from its portfolio before the taxable acquisition can force a gain recognition at the fund level.

Conclusion: The Power of Deferral and Step-Up

The combination of the Section 351 exchange and the ETF’s in-kind redemption mechanism ensures that you are not forced to pay the capital gains tax when the merger or take-private deal closes.

- Deferred Gain: The capital gain is deferred until you, the investor, eventually choose to sell your shares of the diversified ETF.

- Compounding Power: The money you would have paid in taxes remains invested and continues to compound in the ETF.

- Potential Step-Up in Basis: If you hold your ETF shares until your death, your heirs will receive a step-up in basis to the fair market value at the time of death, potentially avoiding the capital gains tax on that appreciation entirely.

The 351 ETF conversion is a sophisticated and highly effective strategy that transforms an involuntary taxable event into a voluntary, deferred one, preserving capital and maximizing long-term returns.