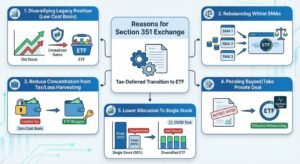

In today’s market, where many long-term investors hold highly appreciated stock portfolios, the prospect of selling to diversify is often met with the potential of a massive capital gains tax bill. A solution has emerged in the form of the Section 351 ETF Exchange, an innovative application of the U.S. tax code that enables investors to exchange their appreciated assets for shares in a new Exchange Traded Fund (ETF) on a tax-deferred basis.

For an ETF issuer looking to capitalize on this growing demand and attract significant assets through a 351 exchange, the design of the new fund must be meticulously crafted. It’s not enough to be just any ETF; the fund’s mandate must offer a clear, compelling diversification upgrade while aligning perfectly with the strict IRS requirements.

1. The Core Value Proposition: Extreme Diversification

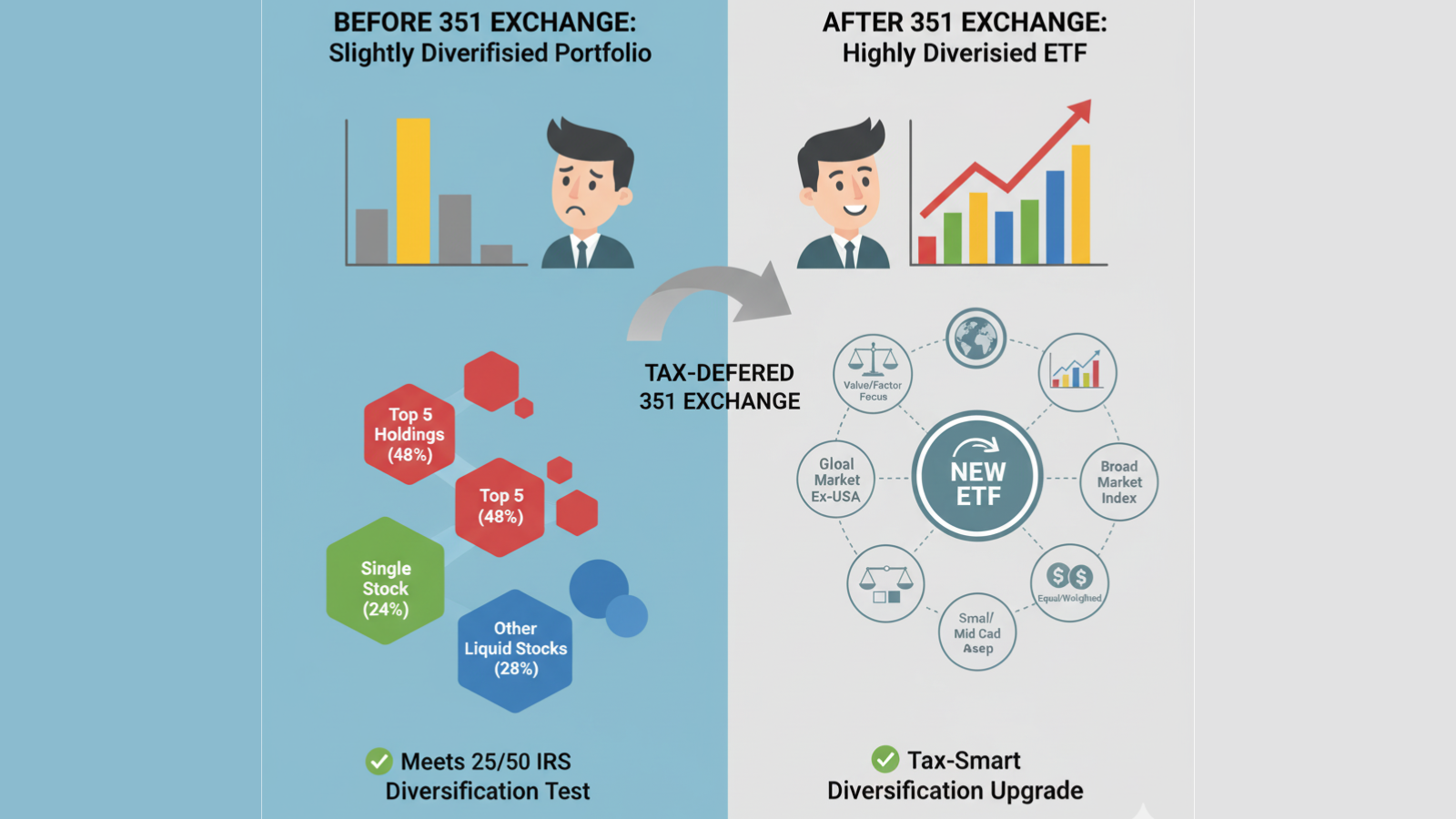

The fundamental appeal of a 351 exchange is the transition from a slightly diversified portfolio—one that meets the minimum pre-transfer requirements—to a highly diversified one.

Investors must contribute a portfolio that is already diversified according to the IRS’s 25/50 Test to qualify for tax deferral:

- No Single Asset Exceeds 25%: No more than 25% of the contributed value can be the stock or securities of a single issuer.

- Top Five Holdings Do Not Exceed 50%: The value of the top five holdings cannot exceed 50% of the total portfolio value.

While the incoming assets are already diversified enough for the IRS, the new ETF must offer the kind of broad, immediate diversification that motivates the exchange. Therefore, the most appealing new ETFs will be:

- Broadly Scoped: The investment strategy should be far-reaching, encompassing a large number of securities, possibly even multi-asset.

- More “Index-Like”: A highly diversified ETF, often tracking a broad-market or multi-factor index, offers a contrast to a contributing portfolio that may have been pieced together just to meet the 25/50 test.

- Not Concentrated: The new ETF must avoid any hint of concentration. A concentrated sector, thematic, or factor ETF is counterproductive to the investor’s goal of risk reduction.

2. Targeting Current Investor Needs: The Escape from Large-Cap Growth

Many investors utilizing a 351 exchange are attempting to manage the success of the past decade, which has led to disproportionately high capital gains in Large-Cap Growth and Technology stocks. The ideal ETF to accept these assets offers an immediate and tax-deferred pivot into less correlated, less appreciated segments of the market.

Winning ETF Characteristics:

- Value-Oriented: A Value or Factor-Focused strategy provides an effective counterbalance to portfolios that are currently overweight in growth stocks.

- Beyond U.S. Large-Cap: Funds with significant exposure to Small and Mid-Cap stocks offer a powerful dimension of diversification.

- Global/International Exposure (Ex-USA): Integrating international and global stocks immediately addresses the potential U.S. concentration risk inherent in many legacy portfolios.

- Equal-Weighted Strategy: An equal-weighted index, rather than a traditional market-cap-weighted one, naturally reduces the influence of the few mega-cap stocks, offering a truer form of diversification and addressing the ‘hidden concentration’ risk of standard indexes.

By pairing the tax-deferral benefits of Section 351 with a strategically diversified, counter-cyclical investment mandate, ETF issuers can create a truly compelling product that allows investors to move “from diversified to more diversified” without triggering immediate capital gains.