For investors sitting on highly appreciated assets, a Section 351 exchange is a powerful—but often overlooked—tool. It enables investors to contribute assets in-kind to a newly formed Exchange-Traded Fund (ETF), deferring capital gains taxes while gaining the flexibility and tax efficiency of the ETF structure.

Here are the five most common reasons investors use this strategy.

1. Diversifying Legacy Position with Low Cost Basis

Many investors hold long-time winners with extremely low cost basis. These positions have created wealth—but selling them creates a large, immediate tax bill.

The Solution: Contribute the stock into an ETF through a 351 exchange.

The Benefit: The investor receives ETF shares in a tax-deferred transaction and gains instant diversification without recognizing capital gains.

2. Rebalancing Within SMAs

Separately Managed Accounts (SMAs) often accumulate significant unrealized gains. Over time, even well-performing SMAs can become “gilded cages,” where rebalancing or changing strategies triggers meaningful taxes.

The Solution: Transfer the SMA’s holdings into an ETF via a 351 exchange.

The Benefit: Once inside the ETF wrapper, the manager can rebalance using the ETF’s in-kind creation/redemption process, avoiding taxable events for the investor.

3. Diversifying Portfolios Stuck After Years of Tax-Loss Harvesting

Years of successful tax-loss harvesting can drive down a portfolio’s cost basis. Eventually, there may be no losses left to offset future gains, leaving the portfolio effectively “locked up.”

The Solution: Move the appreciated assets into an ETF without realizing gains.

The Benefit: Eliminates tax friction and restores the ability to manage or rebalance the portfolio efficiently.

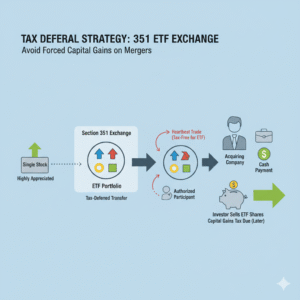

4. Navigating Imminent Buyouts or Take-Private Deals

A sudden buyout often forces investors into a taxable cash-out, even if they’d prefer to maintain exposure or defer gains.

The Solution: Before the deal closes, contribute the diversified portfolio—including the target stock—to a newly formed ETF.

The Benefit: The ETF absorbs the position. Managers can then exit the stock through ETF-specific tools (including “heartbeat” trades) without passing capital gains to the investor.

5. Reducing Single-Stock Allocation

Section 351 can help mitigate concentrated stock positions—but it must pass the IRS’s 25/50 diversification test.

The Constraint:

- No single holding may exceed 25% of the contributed value.

- The top five holdings cannot exceed 50% combined.

A portfolio that is 100% one stock cannot qualify.

The Application:

Investors often pair a large position with a basket of other securities to meet the test—helping reduce concentration risk or sector overweights (e.g., portfolios dominated by Tech).

Summary

A Section 351 exchange is far more than a tax-deferral mechanism. It creates a structural pathway from tax-restricted portfolios—legacy positions, SMAs, concentrated holdings—into the flexible, tax-efficient ETF wrapper. For investors seeking diversification, liquidity, and long-term tax management, it’s one of the most powerful tools available.